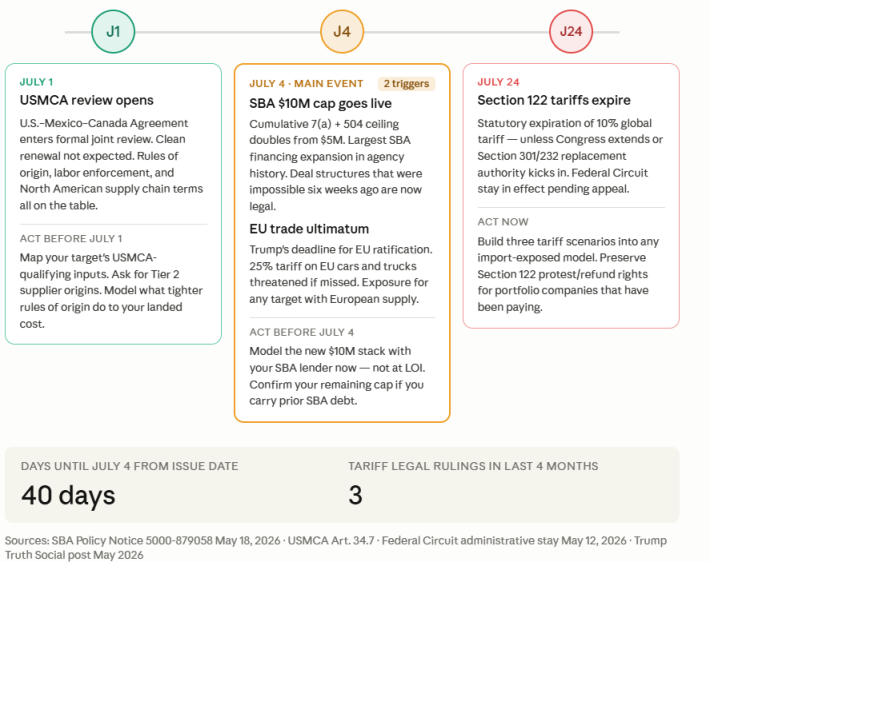

The July 4 Convergence: Three Clocks Are Running at Once

Three separate countdowns are hitting within weeks of each other: SBA's new $10M cumulative loan cap goes live July 4, the USMCA review opens July 1, and Section 122 tariffs expire July 24 unless Congress or replacement authority steps in. Model it now before your next LOI.

Meanwhile, the flash S&P Global Manufacturing PMI for May jumped to 55.3 — the strongest manufacturing expansion since May 2022. That's above the ISM's April confirmed read of 52.7. Two independent surveys are now signaling the same thing: manufacturing is accelerating, not slowing. That matters for valuation and labor underwriting in any industrial deal.

▶SBA doubles cumulative 7(a) + 504 loan cap to $10M — effective July 4 FINANCING / GAME-CHANGER

Buyer read: This changes platform deal math. A buyer stacking a $5M 7(a) acquisition loan with a $5M 504 equipment or real estate add-on has a fully SBA-backed path to a $10M financing package for the first time ever. For anyone underwriting a manufacturing tuck-in or facility purchase, model the new cap before your next LOI. This is not a minor procedural update — it's a structural shift.

▶SBA Patriot Pitch Competition: $1M in non-dilutive prizes — apps close June 10 CAPITAL / OPPORTUNITY

Operator read: If you own or operate an SBA-funded acquisition and have a story worth telling, this is non-dilutive capital with a national platform attached. Four evaluation criteria: strengthening U.S. competitiveness, demonstrating innovation, creating economic opportunity, and showing execution readiness. The June 10 deadline is 18 days away — worth 30 minutes to evaluate eligibility.

▶S&P Global Flash PMI: Manufacturing hits 55.3 in May — strongest since May 2022 MACRO / VALUATION

Buyer read: Two independent surveys, ISM confirmed at 52.7 and S&P Global flash at 55.3, are pointing the same direction: manufacturing is in genuine expansion, not a bounce. For buyers underwriting a manufacturer in the $500K–$3M EBITDA range, rising output and lead-time expansion are tailwinds for forward revenue. The flip side: delivery time lengthening signals supply chain friction that needs stress-testing target by target.

▶Federal Circuit stays CIT Section 122 ruling — tariff legal battle enters next phase TARIFFS / LEGAL

Diligence read: Do not model tariff relief into any acquisition target's forward margin today. The administration has now substituted tariff authority three times in four months. The correct diligence posture is to model three tariff scenarios: current rate, zero if the appeal succeeds, and replacement authority that could be higher under Section 232. Ask the seller how margin moves across all three.

▶USMCA review opens July 1 — North American supply chain assumptions at risk SUPPLY CHAIN / M&A

Diligence read: For any target with Mexican or Canadian inputs — components, subassemblies, materials — the rules of origin assumptions underlying their cost model may shift. USMCA-qualifying inputs currently enter the U.S. duty-free. If tightened rules of origin disqualify existing supplier relationships, tariff exposure can materialize on inputs previously assumed clean.

▶Trump gives EU until July 4 to ratify trade agreement — 25% auto tariff threat TARIFFS / TRADE

Operator read: July 4 is now carrying three simultaneous deadlines: SBA's new loan cap, USMCA review opening, and the EU trade ultimatum. Any acquisition target with European supplier or customer exposure needs a tariff scenario model. The 25% auto tariff threat has direct implications for lower-tier automotive suppliers in the U.S. manufacturing base.

▶SBA $50M Made in America Manufacturing Grant — May 6 announcement MANUFACTURING / GRANTS

Buyer read: For buyers acquiring a manufacturer, the financing stack is genuinely favorable right now: SBA fee waiver, new $10M cumulative cap, Manufacturing Guarantee program, and the International Trade Loan for relevant situations. Ask your lender to model the all-in cash-to-close under the stacked programs before any LOI.

▶Business formation at record highs, Q1 manufacturing job growth returns LABOR / MACRO

Buyer read: Record business formation creates a dual tension: more startups means more future competition for customers, but also more motivated sellers as boomer-owned businesses overlap with demographic handover. ISM and S&P are measuring different cohorts. Watch both. The divergence tells you something about where Main Street sits versus large-cap manufacturing.

IBISWorld Baseline: Landscaping Services in the US represents roughly $188.8B in revenue, ~13.1% profit margin, more than 692,000 enterprises, and nearly 1.5 million employees. The industry remains one of the most fragmented local-service categories in the country, with the four largest players controlling less than 5% of market share.

Operator Summary: Landscaping has quietly evolved from “mow-and-blow” into a much broader recurring-services industry with strong route density economics, commercial maintenance contracts, snow removal, irrigation, arborist work, and premium outdoor living projects. The better operators increasingly resemble field-service businesses more than traditional contractors — dispatch optimization, CRM systems, route density, online reputation, technician retention, and recurring maintenance agreements now matter as much as landscaping quality itself.

Diligence Watch: This is still a labor-heavy operational business with low barriers to entry and heavy local competition. Buyers should underwrite route density, crew utilization, customer retention, seasonal cash flow swings, snow-removal dependency, immigration/labor exposure, equipment replacement cycles, and owner involvement in estimating or sales. Google reviews, recurring maintenance contracts, irrigation capabilities, fleet condition, chemical/fertilizer cost pass-throughs, and concentration in HOAs or commercial accounts matter far more than headline revenue growth.

Valuation Range: Smaller owner-operated residential landscaping businesses still commonly transact in the ~2.5x–4.0x SDE range, particularly where customer relationships are owner-dependent. Larger commercial-focused operators with recurring maintenance contracts, snow management revenue, irrigation services, or multi-crew infrastructure can move into ~4x–6x EBITDA territory.

SBA & Ownership Dynamic: Landscaping continues to fit well inside SBA acquisition economics because of fragmented ownership, recurring maintenance cash flow, aging owner demographics, and relatively low capital intensity. The opportunity for many searchers is operational discipline: digitizing scheduling, improving route efficiency, professionalizing sales, layering in recurring maintenance agreements, and executing tuck-in acquisitions to improve local density.

Labor Market Angle: Labor remains the largest structural constraint in landscaping. The industry relies heavily on seasonal labor and H-2B visa availability, while tightening immigration enforcement and workforce shortages continue to pressure operators. Retaining reliable crew leaders and drivers is increasingly becoming a competitive advantage.

Climate & Sustainability Impact: Climate volatility is reshaping landscaping demand. Drought-prone regions are accelerating adoption of native plants, xeriscaping, drip irrigation, and sustainable hardscaping materials, while warmer winters can reduce snow-removal revenue volatility in some markets. Operators should still stress-test water regulation exposure, fertilizer and chemical inflation, fuel costs, and weather sensitivity before LOI.

Belvertude Joseph on Staffing Stability, Census Discipline, and Why Senior Living Is Not Passive Real Estate

Most people hear “senior living operations” and think occupancy rates and real estate. Belvertude Joseph hears staffing stability, move-in assessments, compliance gaps, resident experience, and operational discipline.

Over the last decade, Bella has worked across assisted living, home healthcare, and multi-site senior living operations — helping facilities stabilize census, improve culture, and navigate the operational chaos that often sits underneath the financial statements.

Bella: “Operations is not about sitting in your office. You need to be in and out of the building, connected to staff, residents, and compliance. Long-term performance comes from operational discipline and visibility.”

Bella: “A lot of operators see 80% occupancy on paper and assume everything is healthy. But you need the real 80%. Move-ins and move-outs must match the system. If the numbers don’t align, you don’t really know your business.”

Bella: “Move-outs, move-ins, assessments, and staffing stability.”

Bella: “Culture. No favoritism. Open-door leadership. Listening to employees the same way you listen to residents. Staff want to feel heard.”

Bella: “Many investors think it operates like traditional real estate. It doesn’t. This is operationally intensive. You need compliance, staffing alignment, culture, resident care, and financial discipline all working together.”

Bella: “Look at census quality, payroll taxes, staffing stability, referrals, and whether the numbers on paper actually match the system. You need to verify the real operational performance.”

The $10M Stack — How to Actually Model the New SBA Cap Before Your Next LOI (~5 min)

The May 18 rule change didn't just raise a ceiling. It changed the math on deals you've already ruled out. A buyer who knows how to stack the programs correctly can now finance an $8M acquisition on almost entirely SBA paper — with real estate or equipment in the mix — and walk away with $300K–$700K less cash out of pocket than six weeks ago. Here's the worked example.

Read full note →The July Countdown — What Acquisition Buyers Need to Do Before July 4 (~6 min)

You've got three calendar invites stacking up on the same day. One is the most significant SBA financing change in agency history. One is a trade agreement review that could reprice your target's entire cost structure. One is a tariff legal situation that has changed every month for four consecutive months and is about to change again. The difference from a normal scheduling conflict: you actually have time to prepare for all three. You just have to start now.

Read full note →Managing Partner / California CPA Operator

Lead an established Los Angeles CPA firm as the day-one managing partner after acquisition.

President, Facility Services & Commercial Construction Platform

Run a $10M+ programmatic facility services and commercial construction platform post-close.

Advisor Role, Food & Beverage Franchising

Join Earned Equity as an industry advisor for a quickservice multi-unit franchise acquisition.

Regional Exit Advisor

Own and grow local Main Street deal flow across assigned markets, from seller engagement through close.

Head of Partnerships

Extend partnerships and build national channels that produce signed seller engagements.

Head of Commercial Real Estate

Build Unbroker's CRE strategy, broker-partner network, policies, compliance, and revenue execution.

More opportunities are live on the full board.

View all opportunities →Upcoming SMB events worth tracking.

SMB Event Radar is built for conferences, webinars, lender events, search fund meetups, operator workshops, broker gatherings, and other calendar-driven links readers can act on.

Boston's largest B2B trade show and networking event for small business owners and entrepreneurs — workshops, exhibitors, keynotes, and speed networking at the Westin Seaport.

Networking lunch for women in tech hosted by Ann Arbor SPARK — elevator pitch practice, speaker development, and community building at Venue by 4M.

One-day summit presented by Access Health CT — panels on marketing, AI, and finance, plus networking and one-on-one consultations at Water's Edge Resort & Spa.

Cocktail mixer for Philly entrepreneurs and small business owners at the Pyramid Club, 52nd floor — relaxed format, multi-industry, open connections.

Rooftop networking mixer for founders, owners, and operators at Blu33 NYC — industry-tagged check-in so you connect with the right people, not just anyone in the room.

The July 4 convergence.

Forty days. Three deadlines. One lender call, one supply chain audit, one customs attorney. Pick your order — just don’t pick none.